Check out our Buy to Let hub.

Non-Owner Occupiers and First-Time Buyers are defined as customers who will not own and reside in a UK residential property on completion. The criteria referenced on this page applies to both small and portfolio landlords.

Please note this also covers policy in relation to Buy to Let like for like remortgage customers.

Our Buy to Let affordability assessment will consider both personal income and expenditure, along with a rental Interest Coverage Ratio (ICR) calculation.

Please use our calculator to check the maximum we can lend.

Portfolio Landlords only (4 or more mortgaged Buy to Let UK rental properties, following completion of this mortgage application. All BTL properties owned individually, jointly or through a SPV / limited company (20% or more shareholding) must be taken into account, including: Consent to Let properties, Holiday lets and HMOs)

If the applicant has a Buy to Let property held within a limited company/SPV, please see Keying the application.

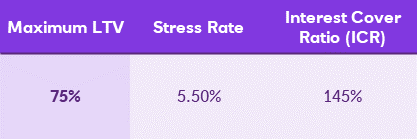

Where the customer is a portfolio landlord we will asses the customer's existing portfolio to ensure the aggregate LTV and ICR is sustainable. The following rental calculation and maximum LTV will apply across your customer's portfolio excluding the property to be mortgaged.

Please note, we will validate the customers estimated rent and capital on all background properties.

Please note - we don’t lend into retirement for First-time Buyers and Non-Owner Occupiers. This includes where they are already retired.

Portfolio landlords only - at least one applicant must have at least 2 years landlord experience.

We don’t allow Top Slicing on this type of application.

Max Portfolio

Portfolio landlords with 10 or less Buy to Let or Consent to Let properties at completion may be considered. This includes all Buy to Let properties, whether mortgaged or unencumbered, owned personally or via SPV / limited company (20% or more shareholding), including Holiday lets and HMOs, and those owned solely or jointly.

Max age

Max age 80 at the end of the term or the customers intended retirement age if this is sooner. We don’t lend into retirement or where the customer is already retired.

Your responsibilities when submitting Buy to Let applications

It is important to key accurate information to avoid delays in the application process. Please ensure that you capture background property addresses, rent, property value, personal income, correct tax band selected (tax band on completion i.e. including all rent), product and product rate.

Please don’t key any rental outgoing the customer has on the affordability calculator or mortgage application.

Please see our packaging requirements for full details. Our underwriters may request additional information if required.

If the customer owns four or more Buy to Let or Consent to Let mortgaged properties on completion of this application we will also require: